Es por tanto el complemento perfecto a cualquier sistema tendencial sobre acciones, futuros, divisas, etc.... donde nuestra estrategia sea direccional.

Aquí nosotros deseamos todo lo contrario, que el mercado se quede totalmente parado y podamos ingresar nuestra prima semanal.

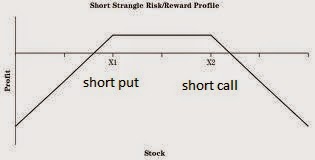

El instrumento que vamos a utilizar es una cuna vendida sobre el índice Russell 2000 ( es incluso mas líquido que el propio S&P 500 por lo que la horquilla es muy cerrada ), donde básicamente vendemos una put y una call fuera del dinero en distintos strikes, sin cobertura alguna; con el claro objetivo que el mercado no se mueva hacia ninguno de los dos extremos.

La forma de ejecutar la venta de la cuna es la siguiente:

Abriremos la posición los jueves (o algunos viernes en caso de dato de empleo) sobre el vencimiento semanal de la semana siguiente (jueves). Estariamos positivos de Theta (valor temporal), pero el resto de las griegas, nos perjudicarían. y tendrían valor negativo para nosotros: delta ( variación en el precio del Indice Russell 2000), gamma ( velocidad con la que lo hace) y vega ( incremento de la volatilidad del índice ).

Deberíamos ingresar como mínimo una prima de 3$ a 15$ ( dependiendo del precio del subyacente y la volatilidad histórica del indice) ; que teniendo en cuenta que estas opciones tienen un multiplicador de 1x100, nos generaría una prima de 400$/1500$ semanal con una garantía en Interactive Brokers de unos 15.000 $ para un contrato en una cuenta REG-T, y algo menos de la mitad en una cuenta Margin Portfolio, pero en la que es necesario un capital minimo de 110.000$.

Jamás esperaremos a que la opción venza y nos la liquiden, como muy tarde al martes de la semana siguiente cerraremos la posición a media tarde, recomprando la cuna. Ni que decir que en opciones semanales, con un vencimiento tan cercano, la gamma tiene un impacto dramático en el resultado. Tampoco estaremos en condiciones de hacer ajuste alguno, pero nuestro estrategia siempre llevará un stop loss asociado en el doble de la prima ingresada aproximadamente.

Esto quiere decir que nunca vamos a quedarnos con la totalidad de la prima ingresada, aunque si con gran parte de ella. Tendremos un porcentaje muy alto de operaciones ganadoras, pero las pérdidas serán dolorosas; por lo que evitaremos operar en semanas donde pueda haber noticias de impacto a lo largo del fin de semana.

Para la elección de los strikes utilizaremos modelos probabilísticos, donde manejemos al mínimo probabilidades cercanas al 70% a vencimiento, que será superiores si cerramos la posición antes.

Para esta primera semana, vamos a detallar los pasos día a día, para una mejor comprensión. Planteamos la operación de la siguiente manera para el vencimiento del 19 de Marzo.

Apertura posición Jueves 12 de Marzo (Venta Cuna):

VALOR INDICE: 1230

STRIKES DE LA CUNA: 1200-1260

INGRESO NETO PRIMA: 5.34$

Cierre posición Martes 17 de Marzo (Compra Cuna):

VALOR INDICE: 1237

RECOMPRA NETA DE LA CUNA: 2.13$

BENEFICIO NETO POR CONTRATO: 321$

VALOR INDICE: 1230

STRIKES DE LA CUNA: 1200-1260

INGRESO NETO PRIMA: 5.34$

Cierre posición Martes 17 de Marzo (Compra Cuna):

VALOR INDICE: 1237

RECOMPRA NETA DE LA CUNA: 2.13$

BENEFICIO NETO POR CONTRATO: 321$

A pie de cada entrada; ire actualizando los registros de datos semananales en una hoja excel, en la que seguiremos un estricto control de money management basado en las ideas de Ryan Jones; para estrategias con un alto porcentaje de aciertos. Empezaremos con 5 contratos y unas garantías de 75.000$ para ua cuenta REG-T en Interactive Brokers.

-----------------------------------------------------------------------------------

We will show through this blog, week after

week, that options are not so difficult to trade and allow us to make money

on a recurring basis if we are disciplined and methodical. Options are complex derivatives that allow us to undertake many strategies with

them, but we will only work

from the sell

side. This means we will look for a weekly credit,

whenever our filters required are met, seeking the laterality of the market.

Therefore it's the perfect complement to any trend system for stocks, futures, currencies, etc .... where our strategy is to bet that the market will move somewhere.

Here we want the opposite, the market must remain completely quiet, in order to be able to cash the premium.

The instrument that we use is a short strangle on the Russell 2000 Index (it's even more liquid than the S&P 500 ), where we basically sell a put and a call out of money at different strikes, uncovered (don't think in iron condors strategies ); with the clear objective that the market does not move toward either extreme.

How to execute the strangle :

We will open the position every Thursday evening on the maturity of the following week ( or some Fridays in case of unemployment rate publication ) , considering that evening we would have credited most of the weekend time value (Theta), which is the only Greek with positive value.. The rest of the Greeks harm our position. and have negative value for us: delta (change in the price of the Russell 2000 Index), gamma (how fast the Index changes) and vega (volatility increase in the index).

We should credit at least 3$/13$ ( depending on the underlying asset value and Index historical volatility ) ; considering these options have a multiplier 1x100, we would generate a real credit of 300$ /1500$ every week with Interactive Brokers margin requirements about $ 15,000 per contract in a REG-T account, and just under half in a Portfolio Margin account ( in this last case 110.000$ of capital is required).

Never wait until the option expires, not later than Tuesday of the following week will close the position at mid-afternoon, buying to cover both options. Needless to say that trading with weekly options, considering the expiration so close, gamma has a dramatic impact on the outcome. Nor will we be able to make any adjustments. Anyway our strategy will be always executed setting a stop loss level (doubling the cashed premium usually ) to prevent us from a market crash

This means that we will never reach the maximum pofit ( 100% of the net credit), but at least a nice bunch of cents. We will have a very high percentage of winning trades, but losses will be painful; so we will avoid operating in weeks where there may be news throughout the weekend.

To select the strikes will use probabilistic models, where we manage a probability close to 70% at maturity, which will be higher if we close the position before the expiration.

For this first week, we will detail the steps every day, for a better understanding

Opening position Thursday March 12th (expiration next March 19th):

INDEX VALUE: 1230

STRANGLE STRIKES: 1200-1260

NET PREMIUM CREDITED: 5.34$

Closing position Tuesday March 17th

INDEX VALUE: 1237

STRANGLE REPURCHASE: 2.13$

NET PROFIT PER CONTRACT: 321$

On the other hand we will keep track of the records, considering a classic money management method based on fixed ratio ideas by Ryan Jones. We will begin with 5 contracts

Therefore it's the perfect complement to any trend system for stocks, futures, currencies, etc .... where our strategy is to bet that the market will move somewhere.

Here we want the opposite, the market must remain completely quiet, in order to be able to cash the premium.

The instrument that we use is a short strangle on the Russell 2000 Index (it's even more liquid than the S&P 500 ), where we basically sell a put and a call out of money at different strikes, uncovered (don't think in iron condors strategies ); with the clear objective that the market does not move toward either extreme.

How to execute the strangle :

We will open the position every Thursday evening on the maturity of the following week ( or some Fridays in case of unemployment rate publication ) , considering that evening we would have credited most of the weekend time value (Theta), which is the only Greek with positive value.. The rest of the Greeks harm our position. and have negative value for us: delta (change in the price of the Russell 2000 Index), gamma (how fast the Index changes) and vega (volatility increase in the index).

We should credit at least 3$/13$ ( depending on the underlying asset value and Index historical volatility ) ; considering these options have a multiplier 1x100, we would generate a real credit of 300$ /1500$ every week with Interactive Brokers margin requirements about $ 15,000 per contract in a REG-T account, and just under half in a Portfolio Margin account ( in this last case 110.000$ of capital is required).

Never wait until the option expires, not later than Tuesday of the following week will close the position at mid-afternoon, buying to cover both options. Needless to say that trading with weekly options, considering the expiration so close, gamma has a dramatic impact on the outcome. Nor will we be able to make any adjustments. Anyway our strategy will be always executed setting a stop loss level (doubling the cashed premium usually ) to prevent us from a market crash

This means that we will never reach the maximum pofit ( 100% of the net credit), but at least a nice bunch of cents. We will have a very high percentage of winning trades, but losses will be painful; so we will avoid operating in weeks where there may be news throughout the weekend.

To select the strikes will use probabilistic models, where we manage a probability close to 70% at maturity, which will be higher if we close the position before the expiration.

For this first week, we will detail the steps every day, for a better understanding

Opening position Thursday March 12th (expiration next March 19th):

INDEX VALUE: 1230

STRANGLE STRIKES: 1200-1260

NET PREMIUM CREDITED: 5.34$

Closing position Tuesday March 17th

INDEX VALUE: 1237

STRANGLE REPURCHASE: 2.13$

NET PROFIT PER CONTRACT: 321$

On the other hand we will keep track of the records, considering a classic money management method based on fixed ratio ideas by Ryan Jones. We will begin with 5 contracts

No hay comentarios:

Publicar un comentario